Insurance Term Definitions: A Beginner’s Guide [Infographic]

If you’re unfamiliar with insurance and trying to learn more, there’s one thing you probably noticed right away: there's a lot of special insurance terminology. This can make it challenging for newcomers to dive in and research what they need to know in insurance. We’ve put together a guide to explain the most common insurance terms to help you get up to speed with the industry.

Common Insurance Terms

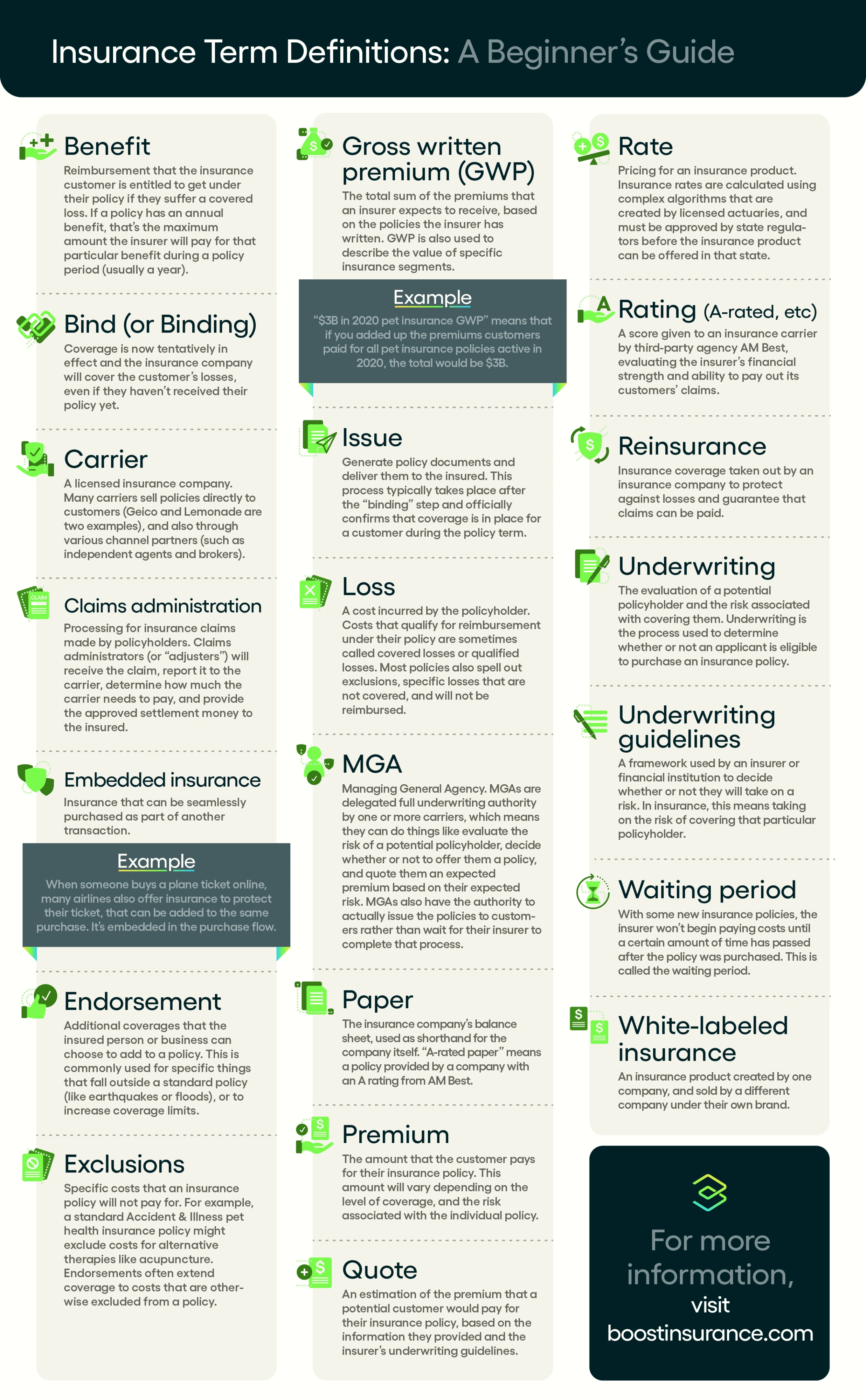

Benefit:

Reimbursement that the insurance customer is entitled to get under their policy. For example, a pet insurance policy would probably include a benefit for accident or illness, meaning that the insurer will cover some or all of the customer’s expenses if their pet gets injured or sick. If a policy has an annual benefit, that’s the maximum amount the insurer will pay for that particular benefit during a policy period (usually a year).

Bind (or Binding):

In insurance, “binding” means that coverage is now tentatively in effect and the insurance company will cover your losses, even if you haven’t received your policy yet.

Carrier:

A licensed insurance company. Many carriers sell policies directly to customers (Geico and Lemonade are two examples), and also through various channel partners (such as independent agents and brokers).

Claims administration:

Processing for insurance claims made by policyholders. If your customer suffers a covered loss, they’ll file a claim for the money they should get under their policy. Claims administrators (or “adjusters”) will receive the claim, report it to the carrier, determine how much the carrier needs to pay, and provide the approved settlement money to the insured. It’s important to note that not just anyone can process an insurance claim. By law, claims administrators and adjusters must be specifically licensed.

Endorsement:

Additional coverages that the insured person or business can choose to add to a policy. This is commonly used for specific things that fall outside a standard insurance policy. For example, a business might add an endorsement to their cyber insurance for social engineering, that pays out if certain employees are tricked into transferring money to a fraudster. Without the endorsement, their cyber insurance policy wouldn’t cover that loss.

Exclusions:

Specific costs that an insurance policy will not pay for. For example, a standard Accident & Illness pet insurance policy might exclude costs for alternative therapies like acupuncture. Endorsements often extend coverage to costs that are otherwise excluded from a policy.

Gross written premium (GWP):

The total sum of the premiums that an insurer expects to receive, based on the policies the insurer has written. GWP is also used to describe the value of specific insurance segments (for example, “$2B in 2020 pet insurance GWP” means that if you added up the premiums customers paid for all pet insurance policies active in 2020, the total would be $2B).

Issue:

Generate policy documents and deliver them to the insured. This process typically takes place after the “binding” step and officially confirms that coverage is in place for a customer during the policy term.

Loss:

A cost incurred by the policyholder. Costs that qualify for reimbursement under their policy are sometimes called covered losses or qualified losses. Most policies also spell out exclusions and specific losses that are not covered, and will not be reimbursed.

Managing General Agency (MGA):

Unlike insurance brokers, who are typically only authorized to sell other carriers’ products, MGAs are delegated full underwriting authority by one or more carriers. This means the MGA can do things like evaluate the risk of a potential policyholder, decide whether or not to offer them a policy, and quote them an expected premium based on their expected risk. MGAs also have the authority to actually issue the policies to customers rather than wait for their insurer to complete that process for them after the fact.

Paper:

The insurance company’s balance sheet, used as shorthand for the company itself. “A-rated paper” means a policy provided by a company with an A rating from AM Best.

Premium:

The amount that the customer pays for their insurance policy. This amount will vary depending on the level of coverage, and the risk associated with the individual policy. For example, a pet insurance policy covering an elderly dog who is more at risk for health issues would likely be higher than a policy covering a puppy.

Quote:

An estimation of the premium that a potential customer would pay for their insurance policy, based on the information they provided and the insurer’s underwriting guidelines.

Rate:

Pricing for an insurance product. Insurance rates are calculated using complex algorithms that are created by licensed actuaries and must be approved by state regulators before the insurance product can be offered in that state.

Rating (A-rated, etc):

A score given to an insurance carrier by third-party agency AM Best, evaluating the insurer’s financial strength and ability to pay out its customers’ claims. This is important: if an insurer has a low rating, it means there’s a risk they may not be able to pay all the benefits their customers are entitled to.

Reinsurance:

Insurance coverage taken out by an insurance company to protect against losses and guarantee that claims can be paid. While reinsurance is complex, the basic concept is a way for insurance companies to share financial risk with the reinsurance companies that back them, increasing overall stability in the insurance market.

Underwriting:

The evaluation of a potential policyholder and the risk associated with covering them. Underwriting is the process used to determine whether or not an applicant is eligible to purchase an insurance policy.

Underwriting guidelines:

A framework used by an insurer or financial institution to decide whether or not they will take on a risk. In insurance, this means taking on the risk of covering that particular policyholder. Outside of insurance, underwriting guidelines apply to financial products like loans (in which the risk is whether or not the borrower will be able to pay). Also called underwriting standards.

Waiting period:

Some insurance policies don’t go into effect immediately. Instead, there is a certain amount of time (for example, a week or a month) that must pass before the insurer will start paying costs. This is called the waiting period. Certain endorsements may come with their own waiting periods, separate from any waiting period that applies to the rest of the policy.

After reading our glossary of insurance terms, we hope you’re feeling more comfortable with the insurance terminology we commonly use in the industry.

Boost makes it easy for any company to get started offering embedded insurance. Learn more about our digital insurance products, or talk to an expert about how embedded insurance can fit into your business.

{kind=link}